It seems we can’t find what you’re looking for. Perhaps searching can help.

It seems we can’t find what you’re looking for. Perhaps searching can help.

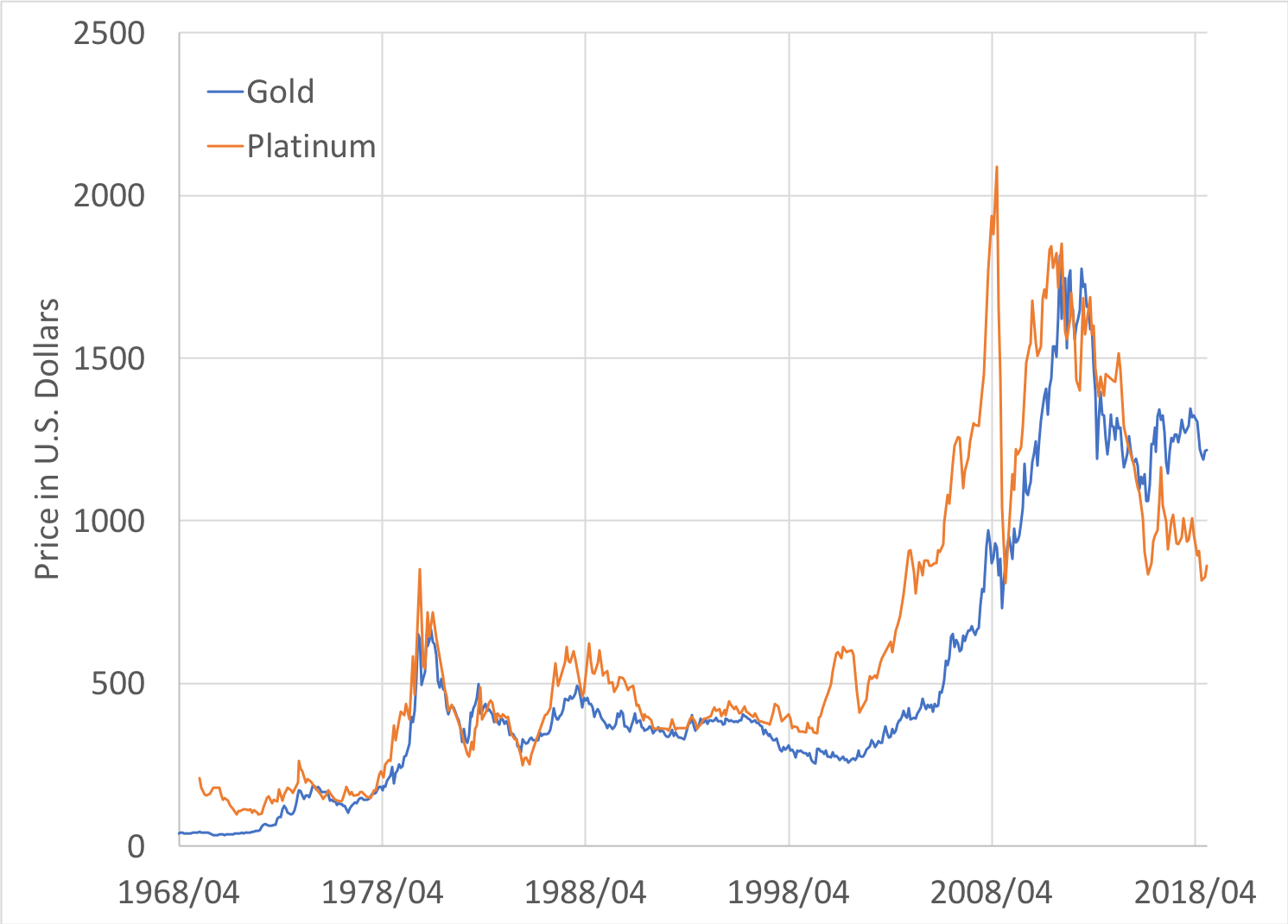

Taxing blockchain forks

The tax treatment of cryptocurrency forks presents four unique challenges: (1) parent/child designation, (2) taxpayer access to the new token, (3) assessment of fair market value, and (4) assessment of comparable contemporaneous fair market values. We provide empirical evidence that each of these issues is a hurdle in determining whether income has been realized, or in apportioning the basis. We consider three existing approaches for assets acquired without a purchase. We conclude that the least problematic approach (adopted by Japan) is giving zero tax basis to the new coin and taxing the proceeds upon a sale, while treating the new coin as realized income (as recently ruled in the US) is the most problematic.

Linking policy to outcomes: a simple framework for debt maturity management

Invited presentations: CEIBS (6/26/2018), HM Treasury (8/30/2018), Federal Reserve Bank of Dallas Banking and Finance Workshop (12/4/2018), University of Colorado Boulder, QWAFAFEW Denver Chapter (5/23/2019), Leeds School of Business (5/24/2019). Conference presentations: OECD Public Debt Management Conference (9/4/2019).

Presentations by coauthor marked with an asterisk (*). Future-dated events are scheduled.

Should the government be paying investment fees on $3 trillion of tax-deferred retirement assets?

Invited presentations: Baruch College* (10/24/2016), Texas A&M Mays School of Business* (10/26/2016), Federal Reserve Bank of Chicago* (11/16/2016), Einaudi Institute for Economics and Finance* (3/22/2017), Federal Reserve Bank of Boston (10/13/2017), MIT GFCP Annual Conference (9/11/2019), Vanguard (10/23/2019). Conference presentations: 2016 Red Rock Finance Conference (Springdale, Utah, 9/9/2016), Lone Star Finance Conference (Texas Christian University, Fort Worth, 9/16/2016), ESSFM Gerzensee (Gerzensee, 7/19/2017), World Finance Conference (Cagliari, 7/27/2017), 2017 DCIIA Academic Forum* (New York, 10/19/2017), 15th Paris December Finance Meeting (Paris, 12/21/2017), European Finance Association Conference (Warsaw, 8/23/2018), CEAR-RSI Household Finance Workshop (Montreal, 11/19/2018).

Presentations by coauthor marked with an asterisk (*). Future-dated events are scheduled.

Does fixed point iteration converge to the correct asset price in dynamic models with taxes?

The price paid for an asset may affect future after-tax cash flows, in turn affecting the value of the asset holding itself. Thus, the price an investor is willing to bid depends on itself recursively, and often an analytic solution is impractical or nonexistent. We discuss the conditions under which fixed point iteration converges to the correct asset price. An intuitive economic interpretation of these conditions suggests that the procedure is generally very safe. However, we present two real-world examples in which iteration need not converge to the correct price, and suggest ways to deal with similar cases.

Do taxes or information drive demand for bond insurance?

I perform the first-ever test of the tax arbitrage theory of bond insurance (Nanda and Singh, 2004) using a complete dataset of all 2015 municipal bond issues. For bonds that are insured in practice, the tax-arbitrage value created by insurance is negligible and, under a realistic calibration, negative. Consistent with this fact, and contrary to the theory’s predictions, taxable municipal bonds are insured as often as tax-exempt ones. Bond insurance is concentrated among small, unrated issues; for the smallest of these, the insurance premium is likely cheaper than rating agency fees. This evidence suggests that insurance creates value by producing information.

Do taxes or information drive demand for bond insurance?

Conference presentations: Lone Star Finance Conference (Baylor University, Waco, 9/15/2017)

Tricks of the trade? Pre-issuance price maneuvers by underwriter-dealers

Tricks of the trade? Pre-issuance price maneuvers by underwriter-dealers

Invited presentations: Midwest Finance Association Conference (3/3/2018), Shanghai Advanced Institute of Finance (7/3/2018), Federal Reserve Bank of New York (8/7/2018), Seoul National University (11/19/2018). Conference presentations: 2018 Western Finance Association* (San Diego, California, 6/18/2018), 2019 American Finance Association (Atlanta, Georgia, 1/5/2019), Finance Down Under* (Melbourne, Australia, 3/8/2019).

Presentations by coauthor marked with an asterisk (*). Future-dated events are scheduled.

Should the government be paying investment fees on $3 trillion of tax-deferred retirement assets?

In a standard benchmark, both individuals and the government are indifferent between traditional tax-deferred retirement accounts and “front-loaded” (Roth) accounts. We add investment fees to this standard benchmark and show that individuals are still indifferent but the government is not. We estimate that, by deferring tax revenue, the U.S. government pays $16.1 billion in annual fees, representing an implicit subsidy to asset managers. We also show that this result continues to hold when asset managers choose the fee level competitively in equilibrium. In our model, tax deferral produces a larger asset management industry, lower tax revenue and lower social welfare.

Loan Terms and Collateral: Evidence from the Bilateral Repo Market

Invited presentations: Federal Reserve Board* (Washington, D.C., 5/26/2015); University of Colorado, Boulder* (10/1/2015); Hong Kong University* (12/14/2015); Peking University HSBC Business School* (16/12/2015); ICEF (Moscow, 6/16/2016); CEIBS (Shanghai, 7/20/2016). Conference presentations: 2015 Lone Star Finance (UT Dallas, 9/18/2015), XXIV International Rome Conference on Money, Banking and Finance (LUMSA, Rome, 12/3/2015), Money Markets and Central Bank Balance Sheets workshop (European Central Bank, Frankfurt, 12/7/2015), 2015 International Dauphine-ESSEC-SMU Conference on Systemic Risk* (ESSEC, Singapore, 12/11/2015), SWFA (Oklahoma City, 3/10/2016 – McGraw-Hill Education Distinguished Paper Award), Financial Management Association Annual Meeting (Las Vegas, 10/20/2016), CAFM 2016* (Seoul, 12/3/2016), Paris December International Finance Meeting (Paris, 12/20/2016), American Finance Association Annual Meeting* (Chicago, 1/6/2017), SFS Cavalcade (Nashville, 5/16/2017), World Finance Conference (Cagliari, 7/27/2017).

Presentations by coauthor marked with an asterisk (*). Future-dated events are scheduled.

Capital gains taxes and trading incentives

Invited presentations: Bank of Italy (Rome, 1/21/2014), Bank for International Settlements (Basel, 1/24/2014), Southern Methodist University (Dallas, 1/29/2014), Federal Reserve Bank of New York (2/28/2014).

Presentations by coauthor marked with an asterisk (*). Future-dated events are scheduled.

Quantifying Tail Risk for Hedge Funds

Conference presentations: NBER-NSF Seminar on Bayesian Inference in Econometrics and Statistics 2013 (St. Louis, 5/4/2013) under the title “Tales of Tails: Quantifying Extreme Downside Risk.”

Presentations by coauthor marked with an asterisk (*). Future-dated events are scheduled.

Quantifying Tail Risk for Hedge Funds

We evaluate popular measures of hedge fund tail risk such as maximum drawdown (MDD) and worst one-period loss, and prove theoretically that realized tail risk is a downward-biased estimator of true tail risk. The bias can be almost 100% using a reasonable calibration. That is, true tail risk can be twice as large as its conventional estimator (realized tail risk). Kelly and Jiang (2013) show that tail events are systematic rather than idiosyncratic, so tail risk cannot be eliminated via diversification. Accurate measurement of fund-level tail risk is therefore essential for loss-averse investors and redemption-averse asset managers. We propose a simple, efficient parametric estimator that needs only short return histories as input and predicts future tail event probabilities and magnitudes with surprising precision. Additionally, we note that using sample standard deviation to estimate volatility is also biased, as originally observed by Miller and Gehr (1978) who provide a correction when returns are normal. The same technique employed in this paper to estimate tail risk can be used to improve estimation of the Sharpe ratio and other measures based on volatility for any return distribution, and in particular when returns (or simply the tails) follow power laws (Gabaix et al., 2006).

Capital gains taxes and trading incentives

Once all present and future tax consequences of a sale are included, the effective tax rate on capital gains and losses is almost always less than the statutory tax rate, and it is asset- and investor-specific. As demonstration, I compute the effective tax rates for taxable and tax-exempt bonds held by property-casualty insurers (0 to 10% versus 15 to 30%) and show empirically that because of the higher effective tax rate, property-casualty insurers are more reluctant to realize gains on tax-exempt bonds, compared to taxable bonds, even though all gains are taxed at a statutory rate of 35%.

Loan Terms and Collateral: Evidence from the Bilateral Repo Market

We study secured lending contracts using a novel, loan-by-loan database of bilateral repurchase agreements in which borrower quality is fixed and collateral quality is known. Holding all risk factors constant except collateral quality, we show that loans on riskier collateral have higher spreads, that is, they remain riskier even though lenders require higher margins. We also document that lower-quality loans have longer maturity, driven by borrower rollover concerns. Our results suggest that maturity is not lenders’ primary risk management tool. Holding loan quality constant (including collateral), we show that one point of spread substitutes for approximately 9 points of margin.

Tax Distortions and Bond Issue Pricing

Brandeis-Bond Buyer 2014 Municipal Finance Conference (Boston, 7/30/2014) and American Finance Association Annual Meetings (Boston, 1/4/2015).

Presentations by coauthor marked with an asterisk (*). Future-dated events are scheduled.

Tax Distortions and Bond Issue Pricing

Original issue premium (OIP) bonds are the norm in the U.S. tax-exempt market, but very rare in the taxable market. A tax subsidy helps explain this disparity. Unlike bonds issued at par or discount, the price of OIP bonds can fall and yet remain above par, providing secondary market buyers with more tax-exempt coupon and less taxable market discount. Investors’ aversion to taxable market discount explains additional, previously undocumented empirical facts. In a calibration exercise, this subsidy’s expected cost to the U.S. Treasury is estimated at $1.7 billion per year.